Simple Ways to Talk to Creditors When You Can’t Pay starts with one hard truth. Ignoring creditors makes everything worse. Fees grow, stress builds, and options disappear fast.

The good news is you don’t need perfect words or special skills. You just need a simple plan and the right way to speak.

Here, you’ll learn exactly how to talk to creditors, what to say, what to avoid, and how to get better payment options even if money is tight.

How to Talk to Creditors

To talk to creditors, contact them early, explain your situation clearly, and ask for specific help like lower payments, reduced interest, or a payment plan. Stay calm, offer what you can afford, and always ask for the agreement in writing.

What Does It Mean to Talk to Creditors?

Talking to creditors means contacting the company you owe money to and asking for better payment terms. This can include lowering payments, reducing interest, removing fees, or setting up a payment plan. You can do this by phone, email, or written request, and it often helps prevent collections.

When Should You Talk to Creditors?

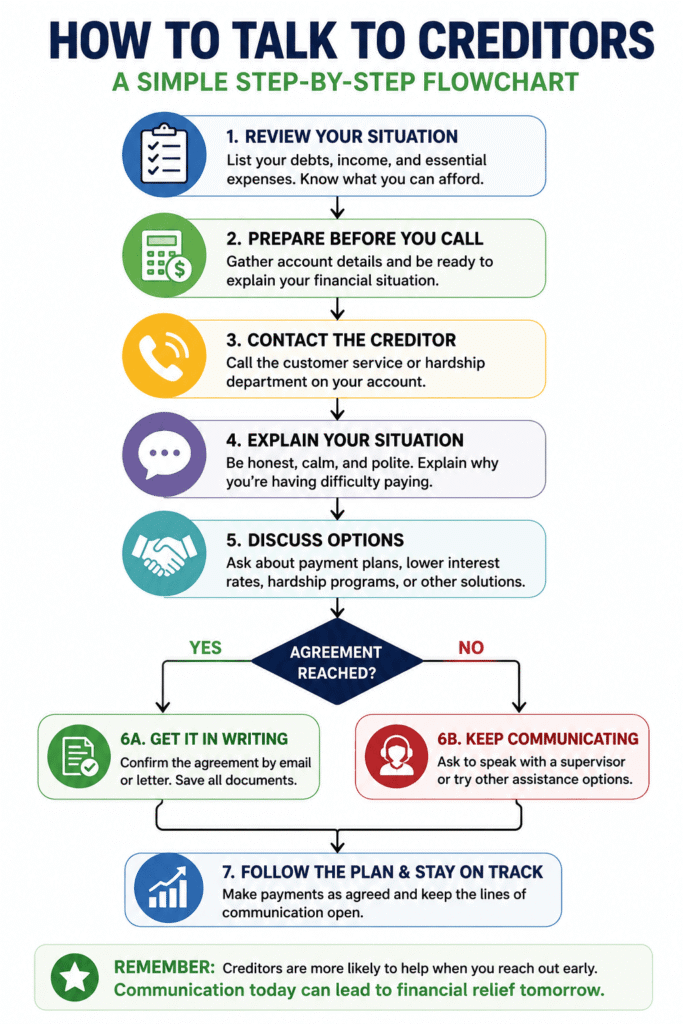

You should talk to creditors as soon as you know you can’t make a payment. The earlier you reach out, the more options you have.

Best times to contact creditors

- Before you miss a payment (highest chance of help)

- Right after a missed payment

- When your income drops or expenses increase

- Before your account goes to collections

Waiting reduces your options. Early action gives you more control.

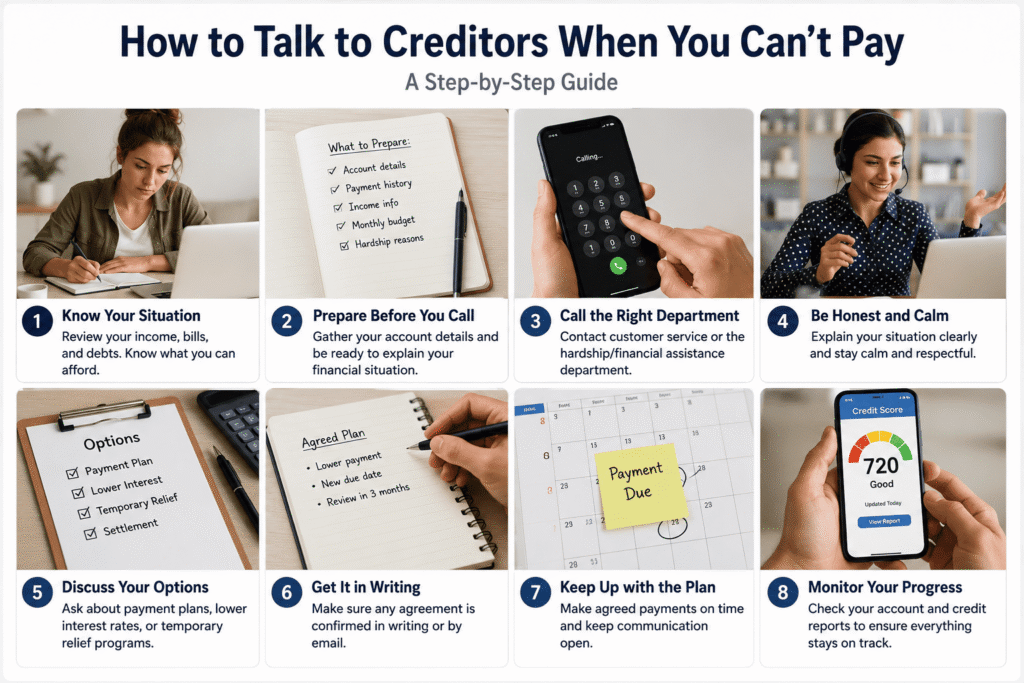

How to Prepare Before You Talk to Creditors

Preparing before you talk to creditors helps you avoid bad deals and stay in control.

Before you talk to creditors, you need a clear picture of your situation. Preparation helps you stay confident and avoid agreeing to payments you can’t afford.

Know your debt details

- Total balance

- Interest rate

- Minimum payment

- Past due amount

- Due dates

Know what you can afford

Look at your real budget. Not guesses.

Pick a payment you can stick to every month.

Set one goal for each call

Don’t try to fix everything at once.

Choose one:

- Lower monthly payment

- Lower interest rate

- Payment pause

- Settlement offer

Gather basic information

- Recent statements

- Income details (if needed)

- Notes from past calls

When you prepare like this, you sound clear and in control—and creditors take you more seriously.

Best Time to Talk to Creditors (Timing Matters More Than You Think)

The timing of when you talk to creditors affects how much help you get. Earlier is always better.

When you have the most power

- Before missing a payment

- Right after a missed payment

- When your situation just changed

When options get limited

- After multiple missed payments

- When the account is in collections

- When legal action starts

If you wait too long, creditors have fewer reasons to help. Early action gives you more control.

11 Simple Ways to Talk to Creditors When You Can’t Pay

Talking to creditors is not about saying the perfect words. It’s about being clear, calm, and knowing what to ask for. These simple steps show you exactly how to talk to creditors and get better results.

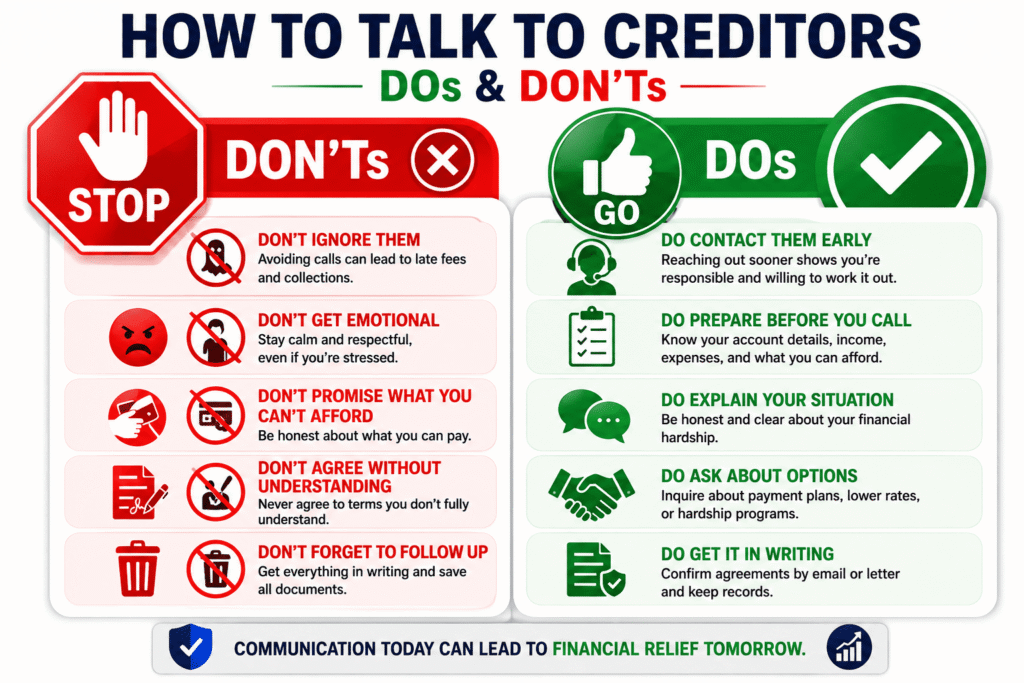

1. Start the conversation early

The earlier you talk to creditors, the more options you have. Waiting leads to late fees and fewer choices.

Say:

- “I’m having trouble keeping up and want to discuss options before I fall behind.”

2. Keep your explanation short

You don’t need a long story. Keep it simple and direct.

Say:

- “My income has changed, and I need help with payments.”

Short answers keep the conversation focused.

3. Be clear about what you want

Don’t wait for them to guess. Ask directly.

Say:

- “I need a lower monthly payment that I can afford.”

Clear requests get better results.

4. Ask about hardship programs

Many creditors have programs but won’t mention them unless you ask.

Say:

- “Do you have any hardship programs available for my account?”

This one question can unlock better options.

5. Ask for a lower interest rate

Interest keeps your balance high. Reducing it helps long term.

Say:

- “Is there any way to lower my interest rate on this account?”

Even small reductions matter.

6. Request fee removal

Late fees add up fast. Many can be removed.

Say:

- “Can this late fee be waived as a one-time courtesy?”

Always ask. It often works.

7. Offer a payment you can afford

Don’t agree to numbers you can’t handle.

Say:

- “I can pay [amount] monthly. Can we set that as my plan?”

Stay realistic. This protects you.

8. Don’t accept the first offer

The first offer is not always the best.

Say:

- “That amount is still too high. Is there a lower option available?”

This is where most people lose money.

9. Stay calm and in control

Tone matters more than words. Stay steady, not emotional.

- Don’t argue

- Don’t rush

- Don’t panic

Calm people get better deals.

10. Ask for everything in writing

Never rely on verbal promises.

Say:

- “Can you send me this agreement in writing?”

This protects you later.

11. Follow up if needed

If you don’t get help the first time, try again.

- Call back later

- Speak to another agent

- Ask for a supervisor

Different people give different options.

These simple ways to talk to creditors give you control. You don’t need perfect words—just clear requests and steady follow-through.

Real Example: How to Talk to Creditors (Step-by-Step Call)

Here’s how a real conversation can go when you talk to creditors.

You:

“I’m calling about my account. I’ve had a drop in income and can’t keep up with the current payments.”

Creditor:

“We can offer a payment plan of $150 per month.”

You:

“That amount is still too high for me. I can afford $90. Are there any lower options available?”

Creditor:

“Let me check… we can reduce it to $100.”

You:

“That’s closer. Can you also reduce the interest or remove any fees?”

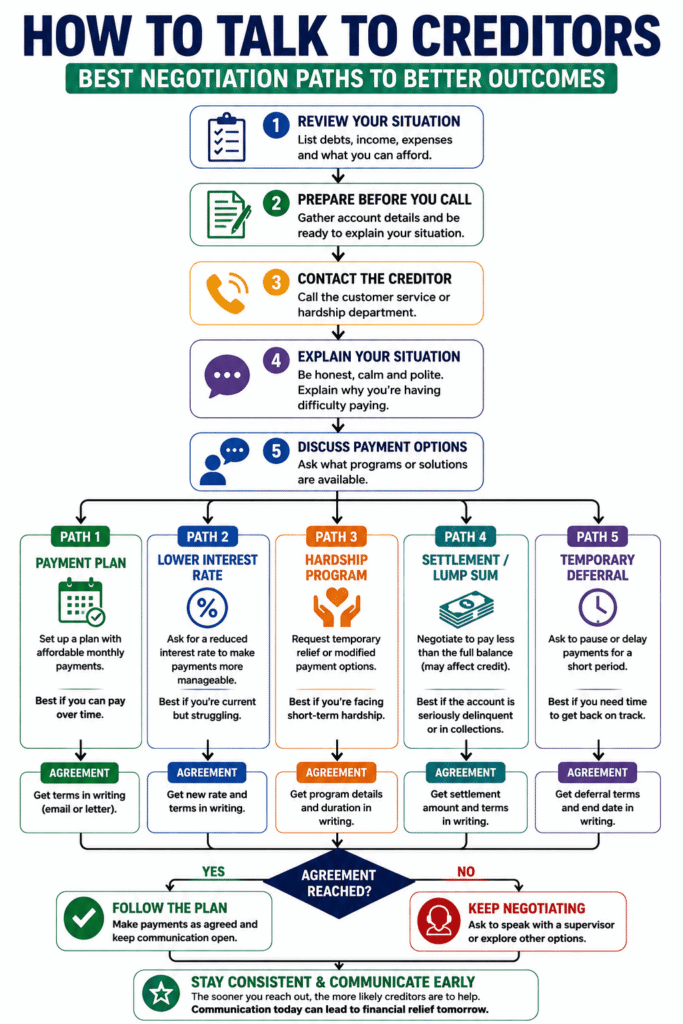

How to Negotiate With Creditors and Get Better Terms

When you talk to creditors, negotiation helps you lower payments and reduce costs.

Negotiation is a normal part of talking to creditors. You are not asking for a favor. You are asking for workable terms.

Keep these rules in mind

- Always ask, never assume

- Focus on what you can pay, not what you owe

- Stay calm and speak clearly

- Pause and let them respond

- Be ready to ask again

Simple negotiation flow

- Explain your situation

- Ask for a solution

- Listen carefully

- Push back if needed

- Confirm details

The goal is simple. Get terms you can actually follow.

What If the Creditor Says No? (Most Important Section)

At some point, a creditor may refuse. This is where most people give up. Don’t.

If they say “we can’t help”

Say:

- “Are there any hardship programs available?”

- “Can I speak with someone who handles payment options?”

If they push for full payment

Say:

- “I want to resolve this, but I need a realistic payment plan.”

If the offer is too high

Say:

- “That amount won’t work for me. Is there a lower option?”

If they refuse again

- Call back later

- Speak to a different agent

- Try again in a few days

Different agents often give different answers.

What Not to Say When You Talk to Creditors

Knowing what not to say when you talk to creditors protects your position.

The wrong words can weaken your position fast.

Avoid these mistakes

- “I’ll pay anything”

- “I promise I’ll catch up soon”

- “Just tell me what to do”

- “I don’t know what I can afford”

These statements remove your control.

Better approach

- Be clear

- Be realistic

- Stick to your limits

Control the conversation, or it controls you.

Common Mistakes When Talking to Creditors

Most people lose money here, not in the negotiation.

Biggest mistakes

- Waiting too long to call

- Not knowing your numbers

- Accepting the first offer

- Agreeing to payments you can’t afford

- Not keeping records

- Ignoring follow-ups

Each mistake makes your situation worse.

How to Talk to Different Types of Creditors

Not all creditors work the same way. Adjust your approach.

Credit card companies

- More flexible

- Often have hardship programs

- Easier to lower interest

Personal loans

- Less flexible

- Focus more on payment plans

Medical bills

- Often negotiable

- Discounts or payment plans are common

Utility companies

- May offer extensions or short-term help

- Limited long-term flexibility

Knowing this helps you ask the right way.

What Happens After You Talk to Creditors

The conversation is not the end. What you do next matters just as much.

After every call or email

- Write down what was agreed

- Save emails and documents

- Check your next statement

- Track your payments

If something looks wrong, contact them again right away.

Can Talking to Creditors Lower Your Debt?

Yes. Talking to creditors can lower your debt in several ways.

- Reduced interest rates

- Removed late fees

- Lower monthly payments

- Settlement offers

But this only works if you ask and follow through.

Why Creditors Are Willing to Work With You

Many people think creditors won’t help. That’s not true.

Creditors prefer:

- Partial payments over no payments

- Avoiding collections costs

- Keeping accounts active

When you talk to creditors, you give them a reason to work with you.

That’s why asking matters.

Can I talk to creditors myself or do I need help?

Yes, you can talk to creditors yourself. Most creditors are open to working directly with you if you explain your situation and ask for options. You don’t need a third party to negotiate, but you do need a clear plan and realistic payment offer.

How do I talk to creditors if I have no money?

If you have no money, talk to creditors as soon as possible and explain your situation clearly. Ask about hardship programs, payment pauses, or reduced payment plans. Most creditors prefer some communication over none and may offer temporary relief until your finances improve.

Can creditors lower your payments if you ask?

Yes, creditors can lower your payments if you ask early and show willingness to pay. Options may include reduced monthly payments, lower interest rates, or hardship plans. Results depend on your account status, but asking directly increases your chances of getting help.

What is the best way to negotiate with creditors?

The best way to negotiate with creditors is to stay calm, explain your financial situation, and request specific changes like lower payments or interest rates. Offer a realistic amount you can afford and don’t accept the first offer if it doesn’t work for you.

What should I say when I call a creditor about debt?

When you call a creditor, say you’re having financial difficulty and want to find a payment solution. Keep it short and clear. Ask about options like lower payments or hardship programs, and take notes of everything discussed during the call.

Will talking to creditors stop collections?

Talking to creditors early can help prevent your account from going to collections. If your account is already in collections, communication can still help you negotiate a payment plan or settlement and may stop further collection actions depending on the agreement.

Can I negotiate my debt myself without a company?

Yes, you can negotiate your debt yourself without hiring a company. Most creditors are open to working directly with you if you explain your situation and make a reasonable offer. Doing it yourself saves fees and gives you more control over the outcome.

What happens if I ignore creditors for too long?

If you ignore creditors, your debt can grow due to fees and interest, and your account may go to collections or legal action. Your credit score will drop, and your options will shrink. Talking to creditors early helps you avoid these outcomes and keeps more solutions available.

Final Thoughts

Talking to creditors is not something to fear. It’s something to use.

The earlier you act, the more options you have. Clear words, simple requests, and steady follow-up can change your situation fast.

Start with one account today. Talk to creditors early, stay clear about what you can afford, and ask for better terms. The sooner you act, the more options you have.