Frugal living tips for families are no longer optional. Rising grocery prices, higher utility bills, and everyday expenses are putting pressure on household budgets. Many families feel stuck between saving money and maintaining a comfortable lifestyle.

The good news is you don’t need extreme cuts to make real progress.

This guide gives you practical, proven ways to reduce expenses, improve family money management, and build long-term stability. You’ll learn simple habits, smart systems, and realistic strategies that work for busy families — not just theory.

What Are Frugal Living Tips for Families and Why Do They Matter Today?

Frugal living tips for families are practical strategies that help reduce unnecessary expenses, improve budget control, and increase long-term savings without lowering quality of life. In today’s economy, where inflation and recurring costs are rising, these systems help families stay financially stable and avoid debt.

Frugal living is not about cutting everything. It is about spending with intention.

Frugal vs Cheap — What Is the Difference?

Frugal means focusing on long-term value, while cheap focuses only on the lowest upfront price. Frugal families consider durability, cost per use, and total ownership cost. Cheap decisions often lead to frequent replacements, increasing long-term expenses instead of reducing them.

Why Frugal Living Matters More in 2026

Frugal living matters more in 2026 because rising grocery prices, higher utility costs, and expanding subscription expenses are increasing financial pressure on families. Without structured budgeting and spending control, household expenses grow automatically, making it harder to save and maintain financial stability.

What Does a Frugal Family Lifestyle Actually Look Like?

A frugal family lifestyle means living below your income, planning expenses in advance, and controlling major spending categories like housing, groceries, and transportation. Most frugal families maintain a 10–20% savings rate while avoiding lifestyle inflation and unnecessary debt.

What Are the Most Common Frugal Living Mistakes Families Make?

Common mistakes include cutting essential expenses instead of waste, failing to track real spending, ignoring irregular annual costs, and attempting extreme budget cuts too quickly. These mistakes often lead to burnout, inconsistent savings, and reliance on debt instead of long-term financial stability.

How Do Frugal Families Save Money Every Month?

Frugal families save money every month by tracking spending weekly, assigning every dollar a purpose, controlling variable expenses, and eliminating recurring waste. With consistent systems like budgeting and expense audits, families can increase their savings rate by 10–20% without reducing essential living standards.

Saving monthly is about structure, not income.

Weekly Budget Tracking System

A weekly budget tracking system helps families control spending by reviewing expenses every seven days instead of waiting until month-end. This approach improves cash flow awareness, prevents early overspending, and allows quick corrections in variable categories like groceries and fuel, increasing overall financial stability.

Zero-Based Budgeting for Families

Zero-based budgeting for families means assigning every dollar of income a specific purpose so that income minus expenses equals zero. Each dollar is allocated to housing, groceries, savings, debt, or sinking funds before the month begins, preventing unplanned spending.

Controlling Variable Spending Categories

Controlling variable spending categories means setting strict weekly limits for flexible expenses like groceries, dining, fuel, and entertainment. These categories fluctuate the most, and managing them actively can reduce total household expenses by 10–20% over time.

Sinking Funds for Irregular Expenses

Sinking funds for irregular expenses are monthly savings set aside for predictable costs like car repairs, holidays, school supplies, and insurance renewals. Dividing annual expenses into monthly contributions prevents financial surprises and reduces reliance on credit cards.

Quick Wins to Save Money Every Month (10 Practical Ideas)

- Set a weekly grocery limit

- Cancel one unused subscription

- Plan meals for 7 days

- Use a spending tracker app

- Combine errands to save fuel

- Review bank statements weekly

- Switch to store brands

- Set a “no-spend” day each week

- Automate savings transfers

- Avoid last-minute purchases

Small actions repeated weekly create real savings.

Deeper Strategy: Why These Systems Work

Most families don’t fail because they don’t earn enough. They fail because they don’t see where money goes. Weekly tracking increases awareness. Budgeting creates control. Sinking funds remove financial surprises.

When these systems work together, spending becomes predictable and savings become consistent.

What Frugal Habits Save the Most Money for Families?

The frugal habits that save the most money for families are cooking at home, planning groceries, eliminating recurring subscriptions, buying secondhand, and tracking spending weekly. These habits target the largest expense categories and can reduce total household spending by 15–25% annually when applied consistently.

Focus on habits that affect big categories.

Cooking at Home as a Primary Cost Reduction Strategy

Cooking at home reduces food expenses because restaurant meals often cost three to five times more than home-prepared meals. Replacing just two dining-out trips per week can save $4,000–$6,000 per year for a family of four.

Structured Grocery Planning

Structured grocery planning means creating a weekly meal plan, setting a budget, and shopping with a list based on sales and pantry inventory. This reduces impulse purchases and food waste, lowering grocery costs by 10–25% annually.

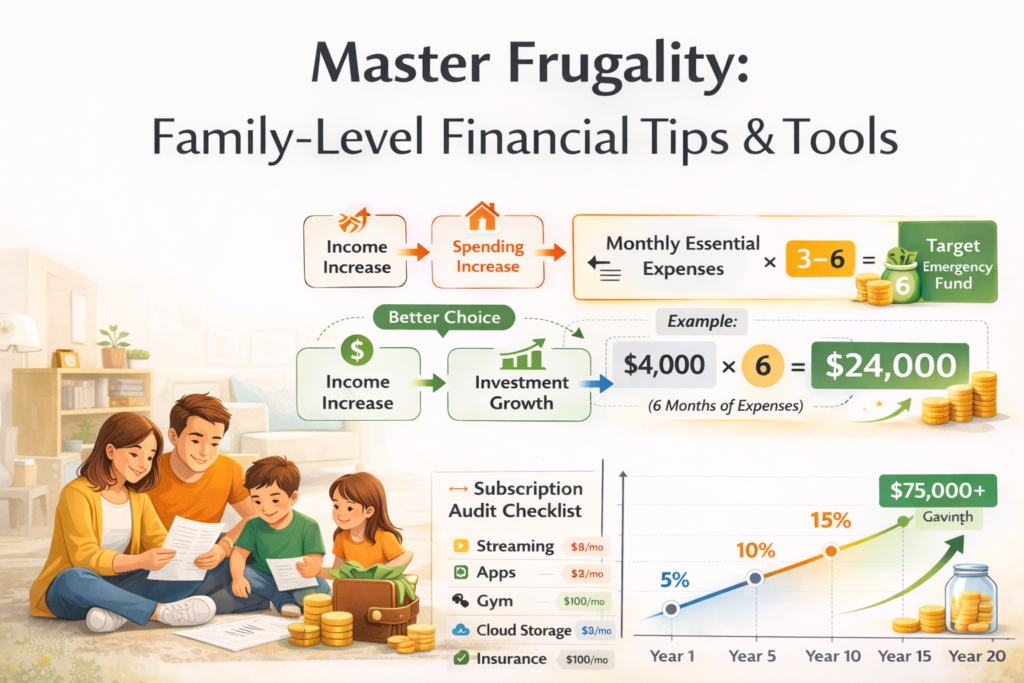

Eliminating Recurring Subscriptions

Eliminating recurring subscriptions removes automatic monthly charges for unused streaming services, apps, and memberships. A simple audit can cut $50–$150 per month, saving up to $1,800 annually without affecting daily life.

Buying Secondhand First

Buying secondhand first means checking resale options before purchasing new items. This reduces costs by 40–70% on clothing, furniture, and household items while maintaining quality and reducing unnecessary spending.

Weekly Spending Awareness

Weekly spending awareness involves reviewing all expenses every seven days. This habit reduces impulse spending and can save $100 per week, which adds up to more than $5,000 annually.

Quick High-Impact Habits (10 More That Work)

- Pack lunches instead of buying

- Use leftovers creatively

- Delay purchases by 48 hours

- Buy in bulk for essentials

- Cancel free trials before renewal

- Limit convenience spending

- Use cashback and discounts

- Plan low-cost family activities

- Set monthly spending limits

- Review subscriptions quarterly

Counterintuitive Insight (Most Families Miss This)

Cutting small expenses like coffee has minimal impact. Reducing large categories like food, housing-related services, and recurring subscriptions creates real savings. Focus on high-impact habits first.

Rare but Powerful Tip

Track cost per use before buying anything over a set amount. This simple rule prevents poor purchasing decisions and reduces long-term spending.

How Can Families Cut Monthly Expenses Fast?

Families can cut monthly expenses fast by eliminating unused subscriptions, reducing dining out, restructuring grocery spending, negotiating bills, and enforcing a short-term spending reset. Targeting high-impact categories first can free up $300–$800 per month within one billing cycle without reducing essential living standards.

Speed comes from focusing on the biggest expenses.

Immediate Subscription and Recurring Expense Cuts

Immediate subscription cuts involve canceling unused streaming services, apps, and memberships. Many families spend $50–$150 monthly on services they rarely use. Removing them creates instant savings without affecting daily life.

Temporary 30-Day Spending Reset

A 30-day spending reset limits expenses to essentials like housing, groceries, utilities, and fuel. This reset reveals spending leaks, improves awareness, and can generate $500–$1,000 in immediate savings.

Reducing Food Costs Quickly

Reducing food costs quickly means cutting dining out, using pantry inventory first, and planning meals around discounts. These changes can lower food spending by 15–30% within a single month.

Negotiating Monthly Service Bills

Negotiating bills for internet, insurance, and mobile plans can reduce costs by $20–$60 per month. Providers often offer discounts when asked, but most families never request them.

Energy and Utility Adjustments

Small changes like adjusting thermostat settings, switching to LED lighting, and reducing idle electricity use can cut utility bills by 5–15% annually while maintaining comfort.

Quick Expense Cuts That Work Immediately (10 Ideas)

- Cancel one subscription today

- Reduce dining out by half

- Call one provider to negotiate

- Set a weekly spending cap

- Turn off unused appliances

- Combine errands to save fuel

- Use a grocery list every trip

- Delay purchases for 48 hours

- Avoid convenience purchases

- Review your last 30 days of spending

Common Mistake Most Families Make

Many families try to cut small expenses first. This wastes time. Real savings come from fixing large categories like food, subscriptions, and recurring bills.

Real-Life Scenario

Imagine saving $150 from subscriptions, $300 from food, and $50 from utilities. That’s $500 per month — $6,000 per year — without changing your lifestyle drastically.

How Can Families Save Money on Groceries for a Family of Four?

Families can save money on groceries for a family of four by using weekly meal planning, buying store brands, reducing food waste, tracking cost per unit, and limiting impulse purchases. These systems can lower grocery expenses by 10–25%, saving $1,500–$3,000 per year without sacrificing food quality.

Groceries are one of the easiest categories to control.

Weekly Meal Planning System

A weekly meal planning system means planning 5–7 meals before shopping and building a grocery list around those meals. This reduces impulse buying and prevents midweek takeout, keeping spending predictable.

Using Store Brands and Cost-Per-Unit Comparison

Using store brands and comparing cost per unit helps families avoid overpaying. Store brands often cost 15–30% less than national brands, and cost-per-ounce comparison prevents misleading “bulk” purchases.

Reducing Food Waste

Reducing food waste means using what you already have before buying more. Most families waste $25–$50 weekly in spoiled food, which adds up to $1,300–$2,600 annually.

Smarter Protein and Ingredient Rotation

Rotating lower-cost proteins like beans, eggs, and lentils a few times per week reduces grocery bills without affecting nutrition. This alone can cut food costs by 10–15%.

Limiting Impulse Purchases

Shopping with a list and avoiding emotional buying reduces unnecessary spending. Even $20 saved per trip can result in $1,000+ per year.

15 Practical Grocery Savings Ideas (That Actually Work)

- Plan meals before shopping

- Buy store brands

- Check price per unit

- Shop once per week only

- Avoid shopping when hungry

- Use a grocery list every time

- Buy seasonal produce

- Freeze leftovers

- Cook in batches

- Rotate cheaper protein meals

- Limit snacks and processed foods

- Use pantry items first

- Compare store prices

- Avoid last-minute store runs

- Track grocery spending weekly

Counterintuitive Insight

Buying in bulk is not always cheaper. If food goes to waste, you lose money. Buy in bulk only for items you consistently use.

Rare Tip Most People Ignore

Track your “cost per meal” instead of total grocery bill. Families that reduce cost per meal gain better control over spending long term.

How Do Frugal Families Create an Accurate Family Budget That Actually Works?

Frugal families create an accurate family budget by tracking real spending, separating fixed and variable expenses, assigning every dollar a purpose, and reviewing the budget weekly. A realistic, data-driven budget improves financial control and can increase savings by 10–20% within a few months.

Accuracy comes from real numbers, not estimates.

Tracking Real Spending Before Budgeting

Tracking real spending means reviewing the last 60–90 days of transactions to understand where money actually goes. Most families underestimate categories like groceries, dining, and subscriptions, which leads to unrealistic budgets.

Separating Fixed and Variable Expenses

Fixed expenses include housing, insurance, and loan payments. Variable expenses include groceries, fuel, and entertainment. Controlling variable categories is key because they offer flexibility and savings potential.

Using Zero-Based Budgeting

Zero-based budgeting assigns every dollar a job so income minus expenses equals zero. This prevents leftover money from being spent impulsively and increases financial discipline.

Building Sinking Funds for Irregular Costs

Sinking funds help families prepare for non-monthly expenses like holidays, repairs, and school supplies. Dividing these costs into monthly contributions prevents budget disruptions.

Weekly Budget Reviews

Weekly reviews help families stay on track and adjust spending before problems grow. Monthly reviews are often too late to fix overspending.

10 Practical Budgeting Tips for Families

- Track expenses weekly

- Set spending limits for each category

- Use a budgeting app or spreadsheet

- Plan for irregular expenses

- Automate savings

- Review subscriptions monthly

- Adjust budget based on real spending

- Avoid “guessing” your numbers

- Keep categories simple

- Focus on consistency, not perfection

Common Mistake That Breaks Budgets

Most families create a budget once and never update it. A working budget must evolve with income, expenses, and lifestyle changes.

Real-Life Example

A family earning $5,000 monthly tracks spending and finds $400 in unnecessary expenses. By reallocating that amount, they increase savings from $300 to $700 per month — more than doubling their savings rate.grading lifestyle, they save $600 and spend $400. Over a year, that builds $7,200 in savings without reducing comfort.

How Can Families Reduce Expenses Without Sacrificing Quality of Life?

Families reduce expenses without sacrificing quality of life by cutting waste instead of essentials, replacing high-cost habits with low-cost alternatives, and improving efficiency in food, utilities, and subscriptions. These changes can lower total spending by 10–20% while maintaining comfort, stability, and family enjoyment.

The goal is smarter spending, not less living.

Replacing, Not Removing, Entertainment

Replacing entertainment means swapping expensive activities with low-cost options like park outings, movie nights at home, or community events. Families still enjoy quality time without overspending.

Optimizing Food Without Lowering Quality

Optimizing food spending involves meal planning, buying seasonal produce, and reducing waste while maintaining balanced nutrition. You spend less without cutting quality.

Managing Utilities and Energy Efficiently

Simple changes like adjusting thermostat settings, using energy-efficient lighting, and reducing electricity waste can lower utility bills without affecting comfort.

Controlling Subscription and Service Costs

Keeping only essential subscriptions and reviewing them regularly prevents unnecessary spending. Most families pay for services they don’t fully use.

Maintaining Value-Based Purchasing

Value-based purchasing means choosing durable, reliable items instead of the cheapest option. This reduces replacement costs and improves long-term savings.

15 Practical Ways to Save Without Feeling Deprived

- Replace dining out with planned home meals

- Use free or low-cost entertainment options

- Limit subscription services

- Shop during sales only when needed

- Plan family activities in advance

- Cook in batches to save time and money

- Use coupons and cashback where practical

- Reduce energy usage during peak hours

- Choose quality over quantity

- Reuse and repurpose household items

- Avoid impulse purchases

- Set limits for discretionary spending

- Plan vacations on a budget

- Share or borrow rarely used items

- Focus on experiences instead of things

Counterintuitive Insight

Cutting everything at once often leads to burnout. Sustainable frugal living works when families keep comfort while removing waste.

Rare Tip Most Competitors Miss

Track “joy per dollar.” If something adds little value but costs a lot, remove it. If it adds high value at low cost, keep it.

How Do Frugal Families Avoid Lifestyle Inflation?

Frugal families avoid lifestyle inflation by keeping core expenses stable as income rises, increasing savings first, and delaying major upgrades. Instead of expanding spending automatically, they protect their savings rate and evaluate long-term costs, which helps build wealth and maintain financial stability over time.

Income growth should strengthen savings, not expenses.

Increasing Savings Before Increasing Spending

Increasing savings first means directing raises or extra income toward savings, investments, or debt reduction before upgrading lifestyle. This prevents income growth from disappearing into higher expenses.

Delaying Major Lifestyle Upgrades

Waiting 60–90 days before upgrading homes, vehicles, or expensive items reduces emotional decisions and ensures purchases are financially sustainable.

Maintaining Budget Discipline After Income Growth

Keeping spending stable after income increases prevents fixed expenses from rising unnecessarily. This preserves flexibility and strengthens long-term financial control.

Teaching Income Discipline to Children

Children who see disciplined spending learn that earning more does not mean spending more. This builds lifelong financial habits.

10 Practical Ways to Prevent Lifestyle Inflation

- Save at least 50% of any raise

- Avoid upgrading lifestyle immediately

- Review expenses after income increases

- Maintain current housing costs if possible

- Set long-term financial goals

- Delay major purchases

- Avoid comparison spending

- Track savings rate regularly

- Focus on needs before wants

- Automate increased savings

Common Mistake

Most families increase spending gradually across multiple categories after a raise. These small increases create permanent higher expenses.

Real-Life Example

A family receives a $1,000 monthly income increase. Instead of upgrading lifestyle, they save $600 and spend $400. Over a year, that builds $7,200 in savings without reducing comfort.

How Do Families Build Long-Term Financial Stability Through Frugal Living?

Families build long-term financial stability through frugal living by maintaining a consistent savings rate, eliminating high-interest debt, planning for irregular expenses, and investing regularly. These systems create predictable cash flow, reduce financial stress, and allow families to grow wealth steadily over time.

Stability comes from consistency, not income alone.

Building a Fully Funded Emergency Reserve

A fully funded emergency reserve covers 3–6 months of essential expenses. This protects families from unexpected events like job loss or medical bills without relying on debt.

Eliminating High-Interest Consumer Debt

Paying off high-interest debt, especially credit cards, reduces financial pressure and frees up monthly income. Interest rates above 15–20% can quickly erase savings progress.

Using Sinking Funds for Predictable Annual Costs

Saving monthly for known expenses like holidays, school supplies, and repairs prevents financial shocks and avoids last-minute borrowing.

Maintaining a Sustainable Savings Rate

Consistently saving 10–20% of income builds long-term financial strength. Even small increases in savings rate compound over time.

Investing for Long-Term Growth

Investing regularly allows families to benefit from compound growth. Even modest monthly contributions can grow significantly over years.

10 Long-Term Wealth-Building Habits

- Save a fixed percentage of income

- Automate savings and investments

- Avoid high-interest debt

- Build emergency reserves

- Invest consistently

- Review finances monthly

- Increase savings with income growth

- Plan for long-term goals

- Avoid lifestyle inflation

- Stay consistent over time

Counterintuitive Insight

You don’t need a high income to build stability. Consistent saving and controlled spending matter more than how much you earn.

Rare but Powerful Insight

Financial stability is built during normal months, not emergencies. Systems created today determine how well you handle future uncertainty.

How Can Families Teach Kids About Money and Frugality?

Families teach kids about money and frugality by modeling responsible spending, involving them in budgeting decisions, using structured allowance systems, and teaching delayed gratification. When children see and practice real financial habits early, they develop strong money skills that carry into adulthood.

Kids learn more from actions than instructions.

Making the Family Budget Visible

Showing children how money is spent on groceries, bills, and savings builds awareness. When kids understand real costs, they make better spending decisions.

Using a Structured Allowance System

A structured allowance divides money into spending, saving, and giving categories. This teaches balance and helps children manage money from an early age.

Teaching Delayed Gratification

Encouraging kids to save before buying helps them understand patience and value. This reduces impulse spending habits later in life.

Involving Kids in Cost Reduction Goals

Including children in saving challenges, grocery planning, or energy-saving efforts builds responsibility and teamwork.

Introducing Teens to Real Financial Tools

Teaching teens to use bank accounts, track spending, and understand basic investing prepares them for financial independence.

10 Practical Ways to Teach Kids About Money

- Let kids help plan grocery lists

- Give a weekly allowance

- Encourage saving for goals

- Discuss family budgeting openly

- Show real bills and expenses

- Involve kids in spending decisions

- Set savings challenges

- Teach basic banking skills

- Explain needs vs wants

- Reward smart money choices

Common Mistake Parents Make

Avoiding money conversations. Kids who don’t learn about money early often struggle with financial decisions later.

Real-Life Scenario

A child saves allowance for a toy instead of buying immediately. This simple habit teaches patience, planning, and long-term thinking.

What Frugal Living Strategies Work Best in 2026?

The most effective frugal living strategies in 2026 combine traditional budgeting with digital tracking, subscription control, flexible spending, and automated savings. Families who monitor expenses in real time and adapt to rising costs can maintain stability, reduce waste, and increase savings despite inflation and economic changes.

Modern frugality is data-driven and intentional.

Digital Budget Tracking Systems

Digital tracking tools help families monitor spending in real time. Weekly visibility prevents overspending and improves financial decisions before problems grow.

Subscription Economy Control

Managing subscriptions through quarterly audits prevents automatic expense growth. Many families overspend due to unnoticed recurring charges.

Cashback and Discount Stacking

Using cashback cards, coupons, and store rewards together increases savings on everyday purchases without changing buying habits.

Flexible Grocery Planning in a Volatile Market

Adjusting meal plans based on current prices and seasonal availability helps control grocery costs during inflation.

Automated Savings and Investment Transfers

Automating savings ensures money is set aside before it can be spent. This builds consistency and removes reliance on discipline.

The 30-Day Frugal Reset Challenge

A 30-day reset eliminates non-essential spending temporarily, helping families regain control and identify wasteful habits quickly.

10 Modern Frugal Strategies That Work Today

- Track spending weekly using apps

- Audit subscriptions every 3 months

- Use cashback on essential purchases

- Automate savings transfers

- Plan groceries based on sales

- Limit digital subscriptions

- Use price comparison tools

- Reduce convenience spending

- Set monthly financial goals

- Review expenses regularly

Counterintuitive Insight

More tools don’t always mean better results. Simplicity and consistency matter more than complex systems.

Rare Insight Most Competitors Miss

Automation is the biggest advantage in modern frugal living. Families who automate savings and tracking outperform those relying on manual discipline.

What Are the Best Frugal Living Ideas for Families? (50+ Practical Ideas)

The best frugal living ideas for families focus on reducing everyday expenses, improving systems, and replacing costly habits with smarter alternatives. By combining daily habits, family activities, home savings, and seasonal strategies, families can consistently lower expenses and build long-term financial stability without feeling restricted.

This is where small actions compound into big results.

Daily Frugal Habits (15 Simple Ways to Save Every Day)

Quick List

- Set 1–2 no-spend days per week

- Plan meals before shopping

- Track spending weekly

- Pack lunches for work and school

- Use leftovers creatively

- Turn off unused appliances

- Set a weekly spending limit

- Delay purchases by 48 hours

- Avoid convenience store stops

- Drink water instead of buying drinks

- Use a shopping list every time

- Limit small daily purchases

- Combine errands to save fuel

- Review daily spending

- Cook at home most days

Deeper Insight

Daily habits control the flow of money. Most overspending happens in small, repeated decisions. Fixing daily patterns creates consistent savings without requiring major lifestyle changes.

Kids & Family Activities (15 Budget-Friendly Ideas)

Quick List

- No-spend weekend ideas (parks, picnics, hikes)

- Family game nights at home

- Library visits and free events

- DIY crafts with household items

- Outdoor sports and activities

- Free community programs

- Movie nights at home

- Budget-friendly family hobbies

- Frugal summer activities for kids

- Low-cost birthday party ideas

- Rotate toys instead of buying new

- Backyard camping nights

- Cooking meals together

- Educational activities at home

- Free online learning resources

Deeper Insight

Entertainment does not need to be expensive. Families that replace paid activities with planned free experiences save hundreds monthly while strengthening family connections.

Home & Lifestyle Savings (15 Practical Ways)

Quick List

- DIY cleaning products recipe

- Frugal home organization hacks

- Declutter and sell unused items

- Buy secondhand furniture

- Repair instead of replacing

- Use energy-efficient lighting

- Reduce water usage

- Batch household tasks

- Save money on kids’ clothes

- Buy off-season items

- Use multi-purpose products

- Share tools with neighbors

- Avoid duplicate purchases

- Maintain appliances regularly

- Reduce laundry frequency

Deeper Insight

Home-related expenses often go unnoticed. Small improvements in efficiency and purchasing decisions reduce long-term costs significantly.

Seasonal & Lifestyle Strategies (15 Smart Ideas)

Quick List

- Frugal holiday traditions

- Budget-friendly gift planning

- Plan expenses for seasonal events

- Frugal homeschool ideas

- Create a family budget binder

- Follow frugal living blogs

- Learn from family success stories

- Start a 30-day frugal challenge

- Adjust spending for inflation

- Plan seasonal grocery shopping

- Set yearly financial goals

- Avoid holiday overspending

- Prepare for back-to-school costs

- Track annual expenses

- Use seasonal discounts

Deeper Insight

Seasonal spending is where many families lose control. Planning ahead turns unpredictable expenses into manageable ones.

Extreme & Advanced Frugal Strategies (High Impact)

Quick List

- Cut one major expense category

- Downsize unnecessary services

- Live below means aggressively

- Reduce fixed expenses long-term

- Track every dollar for 30 days

- Eliminate lifestyle inflation completely

- Use cash-only for variable spending

- Batch cook for entire weeks

- Reduce transportation costs

- Build multiple savings streams

Counterintuitive Insight

Extreme frugality is not required forever. Short-term aggressive strategies can reset finances quickly, then shift to sustainable habits.

Rare Insight Most Competitors Miss

Families who combine systems (budgeting + tracking + planning) outperform those relying only on tips. Systems create consistency. Tips create temporary results.

Beginner to Advanced Frugal Living System

Frugal living works best when families progress from simple habits to structured systems and then to advanced optimization. Starting small builds consistency, while advanced strategies increase savings efficiency and long-term financial stability.

Frugality is a progression, not a one-time change.

Beginner Level (Quick Wins That Work Immediately)

Focus: Awareness + Small Changes

- Track spending for 7 days

- Set a weekly grocery budget

- Cook at home more often

- Cancel one subscription

- Use a shopping list every time

- Avoid impulse purchases

- Start a no-spend day each week

- Review bank statements weekly

Why it works:

These actions create awareness. Most families don’t realize where money goes until they track it.

Intermediate Level (Systems and Consistency)

Focus: Control + Structure

- Use zero-based budgeting

- Build sinking funds

- Set monthly spending limits

- Automate savings

- Plan groceries weekly

- Audit subscriptions quarterly

- Reduce recurring expenses

- Track spending weekly

Why it works:

Systems remove guesswork. Once structure is in place, savings become predictable.

Advanced Level (Optimization and Acceleration)

Focus: Efficiency + Wealth Building

- Increase savings rate to 15–20%+

- Invest consistently

- Eliminate lifestyle inflation

- Optimize major expenses (housing, food, transport)

- Use automation for finances

- Apply cost-per-use thinking

- Run periodic “no-spend challenges”

- Focus on long-term financial goals

Why it works:

At this stage, families shift from saving money to building wealth.

Common Mistake Across All Levels

Trying to do everything at once leads to burnout. Progress works best when changes are gradual and consistent.

Simple Rule to Follow

Master one level before moving to the next. Consistency beats intensity.

How to Start Frugal Living as a Family (Step-by-Step Plan)

Families can start frugal living by tracking spending, identifying waste, building a simple budget, automating savings, and improving one category at a time. This step-by-step approach creates clarity, reduces overwhelm, and builds sustainable money habits that improve financial stability over time.

Start simple. Then improve.

Step 1: Track Your Spending (7 Days Minimum)

Write down every expense for one week. Use a notebook or app.

Focus on groceries, dining, fuel, and small purchases.

Goal:

Understand where your money actually goes.

Step 2: Identify Spending Leaks

Look for unnecessary expenses like unused subscriptions, frequent takeout, impulse buys, or duplicate purchases.

Goal:

Find $100–$300 in easy cuts.

Step 3: Build a Simple Family Budget

Create 4–5 main categories:

- Housing

- Food

- Utilities

- Transportation

- Savings

Assign a limit to each.

Goal:

Control your money before it’s spent.

Step 4: Cut One Major Expense Category

Start with groceries or subscriptions.

These usually offer the fastest results.

Goal:

Create immediate financial relief.

Step 5: Automate Savings

Set up automatic transfers to savings as soon as income arrives.

Goal:

Save first, not last.

Step 6: Introduce Weekly Budget Reviews

Spend 10–15 minutes reviewing expenses every week.

Goal:

Stay on track and adjust early.

Step 7: Improve One Area at a Time

Focus on one category per week:

- Week 1: Groceries

- Week 2: Subscriptions

- Week 3: Utilities

- Week 4: Spending habits

Goal:

Avoid overwhelm and build consistency.

Real-Life Scenario

A family tracks spending and finds $250 in unnecessary expenses. They cut $150 from food and $100 from subscriptions. That’s $250 monthly → $3,000 per year saved with simple changes.

Big Mistake to Avoid

Trying to be perfect from day one. Frugal living works when it becomes a habit, not a short-term effort.

What Frugal Living Mistakes Cost Families the Most Money?

The most costly frugal living mistakes include cutting essential expenses instead of waste, failing to track real spending, ignoring irregular costs, and using extreme budgeting that leads to burnout. These mistakes reduce consistency, increase stress, and often push families back into overspending or debt.

Mistakes don’t just slow progress. They reverse it.

Mistake 1: Cutting Essentials Instead of Waste

Some families reduce groceries, healthcare, or necessary spending too aggressively. This leads to frustration and unsustainable habits.

Fix:

Cut non-essential expenses first, not necessities.

Mistake 2: Not Tracking Real Spending

Without tracking, budgets are based on guesses. This leads to overspending in key areas like food and subscriptions.

Fix:

Track at least 30–60 days of actual spending.

Mistake 3: Ignoring Irregular Expenses

Expenses like holidays, school supplies, and repairs are often forgotten. When they appear, they break the budget.

Fix:

Use sinking funds to plan ahead.

Mistake 4: Trying Extreme Budgeting Too Fast

Cutting everything at once leads to burnout. Families often quit and return to old habits.

Fix:

Make gradual, sustainable changes.

Mistake 5: Focusing Only on Small Expenses

Cutting coffee or small purchases has limited impact compared to groceries, housing, and subscriptions.

Fix:

Focus on high-impact categories first.

Mistake 6: No System or Structure

Relying on willpower instead of systems leads to inconsistency. Without a plan, spending becomes reactive.

Fix:

Use budgeting, tracking, and automation together.

Mistake 7: Lifestyle Inflation After Progress

After saving money, some families increase spending again, canceling their progress.

Fix:

Maintain discipline even when income grows.

Counterintuitive Insight

Being too strict can be just as harmful as not budgeting at all. Balance creates long-term success.

Rare Insight Most Competitors Miss

Consistency beats intensity. Families who make small improvements consistently save more than those who try extreme methods and quit.

Why Frugal Living Works for Families Long-Term

Frugal living works long-term because it creates consistent savings, reduces financial stress, and builds a stable gap between income and expenses. Families who manage money intentionally gain control, avoid debt, and create opportunities for future growth, even without a high income.

It’s not about restriction. It’s about control.

Financial Benefits (What Actually Changes)

- More money left at the end of each month

- Reduced reliance on credit cards

- Ability to handle unexpected expenses

- Increased savings and investment potential

Over time, small savings turn into significant financial security.

Lifestyle Benefits (What Families Feel)

- Less financial stress and anxiety

- Fewer money-related arguments

- More control over daily decisions

- Better planning for the future

Frugal families don’t feel deprived. They feel organized.

Emotional Benefits (What Most People Overlook)

- Confidence in financial decisions

- Reduced guilt around spending

- Stronger family communication about money

- Sense of progress and stability

Money becomes a tool, not a problem.

Long-Term Impact

Families that consistently apply frugal living tips for families often:

- Save 15–25% of income

- Build emergency funds

- Eliminate debt faster

- Invest for future goals

- Avoid financial crises

Real-Life Perspective

Imagine a family that saves $400 per month.

That’s $4,800 per year.

In 5 years → $24,000+ without increasing income.

That’s the power of consistency.

Key Principle

Frugal living is not about doing more.

It’s about doing the right things consistently.

What is the easiest way to start frugal living as a family?

The easiest way to start frugal living as a family is to track spending for one week, identify unnecessary expenses, and reduce one major category like groceries or subscriptions. Starting small builds awareness and creates quick wins, making it easier to stay consistent and improve over time.

How much can families realistically save each month?

Most families can realistically save $200–$800 per month by controlling groceries, reducing subscriptions, and tracking spending weekly. The exact amount depends on income and expenses, but consistent systems can increase savings by 10–25% without major lifestyle changes.

Can frugal living work with kids?

Yes, frugal living works well with kids when families involve them in budgeting, teach basic money habits, and replace expensive activities with low-cost alternatives. Children often adapt quickly and learn valuable financial skills that benefit them long-term.

What are the biggest expenses families should reduce first?

The biggest expenses families should reduce first are groceries, dining out, subscriptions, and recurring service bills. These categories offer the fastest savings potential and can significantly improve monthly cash flow within a short period.

Is frugal living the same as being cheap?

No, frugal living focuses on value, long-term savings, and intentional spending, while being cheap focuses only on minimizing upfront cost. Frugal families prioritize durability, quality, and cost per use to reduce total expenses over time.

How do families stay consistent with frugal habits?

Families stay consistent by using simple systems like weekly budget reviews, automated savings, and clear spending limits. Consistency improves when habits are realistic, repeatable, and focused on long-term goals rather than short-term restriction.

What is the fastest way to reduce financial stress?

The fastest way to reduce financial stress is to cut unnecessary expenses, build a small emergency fund, and track spending weekly. Even small improvements in control and savings can quickly increase confidence and reduce money-related anxiety.

Final Thoughts on Building a Sustainable Frugal Family Lifestyle

Frugal living tips for families are not about extreme sacrifice. They are about clarity, control, and consistent improvement. When families understand where their money goes, reduce waste, and build simple systems, financial stress decreases and stability increases.

You don’t need a perfect plan.

You need a working system.

Start with one category. Improve it. Then move to the next.

Over time, small changes create strong financial habits, and those habits build long-term security. That is how frugal living turns income into stability instead of stress.15 Proven Ways to Save Money Fast on a Tight Budget (Even If You’re Broke)50 Cheap Healthy Meals for Families That Cut Grocery Bills by $300 a Month10 Proven Budget Meal Planning Strategies That Save Families $1,500+ Per Year50 Cheap Healthy Meals for Families That Cut Grocery Bills by $300 a Month