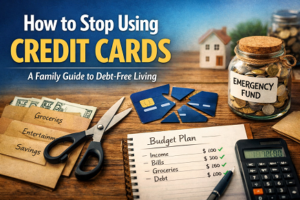

Life rarely goes exactly as planned. A car repair, medical bill, home fix, or sudden job change can hit any family at any time. And when money isn’t set aside, these surprises quickly turn into debt and stress.

The good news: you don’t need a perfect income or complex system to prepare. A simple plan and small consistent steps can protect your family from financial shocks.

Here’s exactly how to budget for unexpected expenses, build an emergency fund, and handle surprise costs without panic.

Let’s make your budget ready for real life.

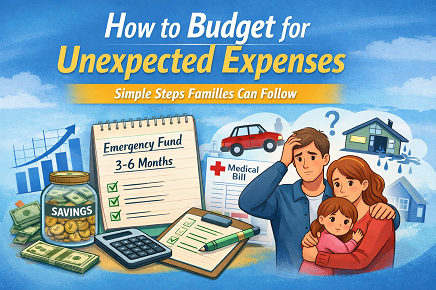

Why Unexpected Expenses Break Most Budgets

Most budgets only cover regular monthly bills. Rent, groceries, utilities, and subscriptions get attention. But surprise expenses get ignored.

Common unexpected expenses include:

- Car repairs or accidents

- Medical bills or medication costs

- Emergency travel

- Home repairs or appliance replacement

- Job loss or income gaps

- School or childcare surprises

When these happen, families often:

- Use credit cards

- Take high-interest loans

- Borrow money

- Delay payments

- Drain savings meant for other goals

A budget that ignores emergencies isn’t complete. Real budgeting includes planning for surprises.

Step 1: Calculate Your Essential Monthly Expenses

First, figure out what your family needs to survive for one month.

Focus only on essentials’:

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Transportation

- Minimum debt payments

- Basic childcare or schooling needs

Ignore entertainment or optional spending for now.

This number shows how much your family needs to stay safe during emergencies.

Example:

- Rent: $900

- Utilities: $150

- Food: $400

- Transport: $150

- Insurance: $100

- Minimum debts: $200

Total essentials: $1,900 per month

This becomes your emergency planning base.

Step 2: Set an Emergency Fund Goal

A common rule is saving 3–6 months of essential expenses.

But families should start smaller if needed.

Smart savings stages:

- Starter emergency fund: $500–$1,000

- One month of expenses

- Three months of expenses

- Six months for stronger security

Small wins matter. A $500 buffer already prevents many debt situations.

Goal example:

Monthly essentials = $1,900

3-month emergency fund = $5,700

Break this into monthly savings targets instead of chasing one big number.

Step 3: Add Unexpected Expenses Into Your Monthly Budget

Instead of reacting to surprises, make them part of your budget.

Add a category like:

- Emergency savings

- Unexpected expenses fund

- Family safety fund

Treat this like a bill you must pay every month.

Even small amounts help:

- $25 per week = $1,300 per year

- $50 per week = $2,600 per year

Consistency beats big deposits.

Step 4: Automate Savings So You Don’t Forget

Manual saving fails because life gets busy.

Automation fixes that.

Best options:

- Automatic transfer on payday

- Separate savings account

- Banking app auto-transfer rules

- Round-up savings features

- Budgeting apps for families

Money saved automatically doesn’t tempt spending.

Make saving happen before you see the money.

Step 5: Cut Small Expenses to Fund Emergency Savings

You don’t need drastic lifestyle changes.

Look for small recurring leaks:

- Extra streaming subscriptions

- Frequent food delivery

- Impulse shopping

- High grocery spending

- Unused memberships

- Expensive phone or internet plans

Redirect those savings into emergency funds.

Small cuts protect your future self.

Step 6: Know What To Do When an Unexpected Expense Happens

When a surprise bill hits, don’t panic.

Follow this order:

- Check if insurance covers it.

- Use your emergency fund first.

- Look for payment plans before using credit.

- Avoid payday loans and high-interest borrowing.

- Adjust next month’s budget to rebuild savings.

Emergency funds are meant to be used. The key is rebuilding them after.

Step 7: Use Budgeting Tools and Apps That Help Families Save

Budgeting apps reduce guesswork.

Helpful features include:

- Spending tracking

- Goal savings tools

- Automatic savings transfers

- Bill reminders

- Family budget sharing

- Expense alerts

Popular budgeting apps and digital tools help families see where money goes and prevent overspending.

But even a simple spreadsheet or notebook works if used consistently.

Tool choice matters less than habit.

Step 8: Build a Family Emergency Plan

Money planning works better when the whole family understands it.

Create a simple emergency plan:

- List emergency contacts

- Keep important documents accessible

- Decide spending priorities in crisis

- Know insurance coverage details

- Assign tasks during emergencies

Planning reduces panic and confusion.

Step 9: Rebuild Your Emergency Fund After Using It

Many families forget this step.

If you spend emergency savings, make rebuilding a priority.

Adjust your budget temporarily:

- Pause optional spending

- Increase savings transfers

- Use extra income to refill funds

- Delay non-essential purchases

Think of emergency savings like a safety net. Repair it quickly after use.

Step 10: Review Your Budget Every Six Months

Life changes. Budgets must change too.

Review savings and expenses when:

- Income changes

- Rent increases

- Family size changes

- Debt is paid off

- Jobs change

Update emergency savings targets regularly.

A budget should grow with your life.

Common Mistakes Families Make

Avoid these budgeting mistakes:

- Waiting to save until income increases

- Keeping emergency money in spending accounts

- Using savings for non-emergencies

- Forgetting to rebuild funds

- Ignoring irregular expenses

Small discipline today prevents big financial stress later.

Simple Action Plan to Start Today

If you only do three things, do this:

- Calculate one month of essential expenses.

- Open a separate emergency savings account.

- Set automatic weekly or monthly transfers.

That’s enough to begin.

Progress matters more than perfection.

Final Thoughts: Protect Your Family From Financial Shocks

Unexpected expenses will always happen. Cars break, homes need repairs, health issues appear, and income sometimes changes.

Families that prepare recover faster and avoid debt.

Start small. Save consistently. Automate what you can. Rebuild savings after using them.

Your future self will be thankful.

Start today: set your first automatic emergency savings transfer, even if it’s small. Small steps build strong financial security.

How do you budget for unexpected expenses effectively?

Start by calculating essential monthly expenses, then save consistently into a dedicated emergency fund. Automate transfers so savings happen every payday. A realistic goal is three to six months of living costs. Regular reviews and small monthly contributions help families handle surprise expenses without relying on debt.

How much should a family save for unexpected expenses?

Most experts recommend saving three to six months of essential household expenses in an emergency fund. Families can begin with a $500–$1,000 starter fund and build gradually. This cushion protects against medical bills, car repairs, or temporary income loss without disrupting the family budget.

What are common unexpected expenses families should prepare for?

Typical unexpected expenses include medical bills, vehicle repairs, home maintenance, emergency travel, appliance replacement, and sudden job loss. Budgeting for emergencies helps families avoid high-interest debt and financial stress when these surprise costs appear throughout the year.

Where should emergency savings be kept?

Emergency savings should be stored in a separate high-yield savings account that is easy to access but not connected to daily spending. Keeping funds separate prevents accidental use while allowing quick access during real emergencies without relying on credit cards or loans.

How can low-income families save for emergencies?

Low-income families can start small by saving weekly amounts, cutting minor expenses, and automating deposits. Even saving $10–$20 per week builds protection over time. Consistency matters more than amount, and gradual savings reduce reliance on debt during unexpected financial situations.

Should unexpected expenses be part of a monthly budget?

Yes. Smart budgets include a category for unexpected expenses or emergency savings. Treating this like a monthly bill ensures money is consistently set aside, making surprise costs manageable and preventing financial setbacks when emergencies occur.

What should you do when an unexpected expense occurs?

Use emergency savings first, check insurance coverage, and request payment plans if necessary. Avoid payday loans or high-interest credit options. After covering the expense, adjust the next budget to rebuild savings quickly, ensuring your financial safety net remains ready for future emergencies.

What tools help families budget for unexpected expenses?

Budgeting apps, automated savings transfers, and expense tracking tools help families monitor spending and build emergency funds consistently. Digital budgeting platforms simplify saving by setting goals, tracking expenses, and sending alerts, helping families avoid overspending while preparing for surprise expenses.

How often should emergency savings goals be reviewed?

Families should review emergency savings and budgets every six months or after major life changes like income shifts, moving homes, or family size changes. Updating savings goals ensures the emergency fund keeps pace with rising living costs and continues protecting against unexpected expenses.